Introduction to Truck Driving as a Career Truck driving isn’t just a job; it’s a lifestyle. For those considering this profession, understanding the ins and outs is essential. Here’s what you need to know. From understanding the nuances of truck...

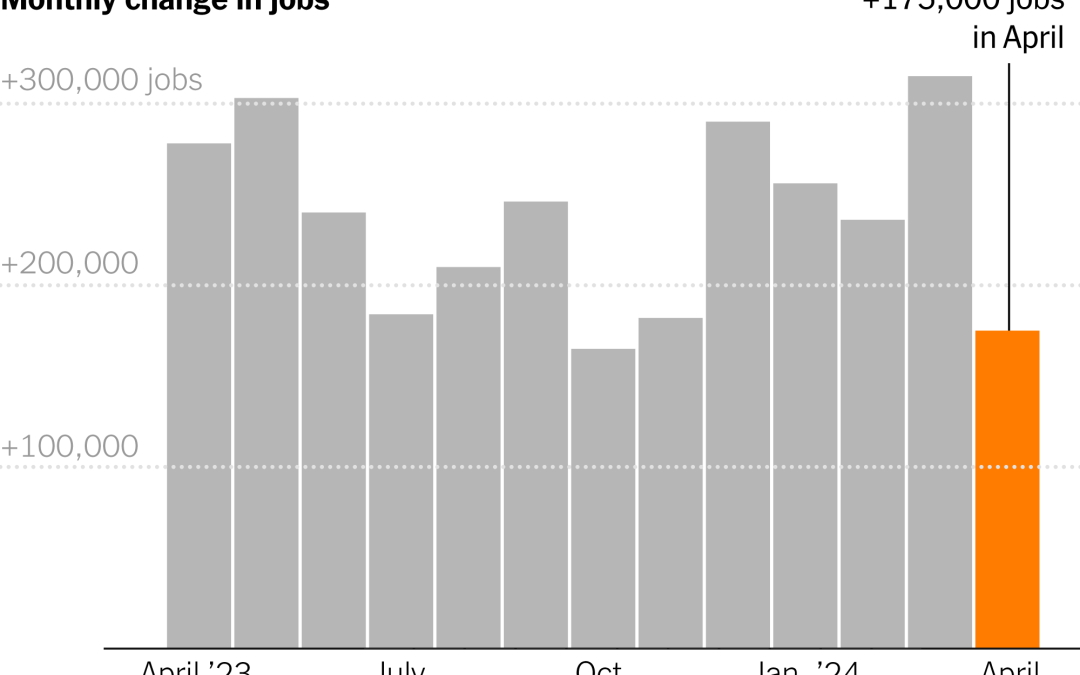

April’s jobs report landed with a thud — only 175,000 jobs were added, pointing to a distinct cooling off from the sizzling pace we’ve seen in recent months. The numbers are more than just digits on a page; they are a harbinger, whispering tales of...

Europe, with its rich history, diverse cultures, and stunning landscapes, is a dream destination for travelers worldwide. From the romantic streets of Paris to the ancient ruins of Rome, the continent offers a plethora of experiences waiting to be discovered. Top...

Chromecast — it’s not just a sleek little device that sits quietly next to your TV. It’s a gateway to a world of endless entertainment, allowing you to stream your favorite videos and audio seamlessly from your phone, tablet, or computer to the big screen....

The cosmos often feels distant, yet it surprises us with connections closer to home than we might expect. Take, for example, the curious case of Kamo’oalewa — a near-Earth asteroid whose story begins not in the far reaches of our solar system, but much closer,...